Homeowners and renters insurance costs now exceed both the rate of inflation and the average rate increases experienced by auto insurance customers during the past year, according to the latest J.D. Power 2024 U.S. Home Insurance Study.

The nationwide surge in rates has driven a sharp increase in the percentage of customers shopping for new policies.

Redesigned in 2024, the study examines overall customer satisfaction within two distinct personal insurance product lines: homeowners and renters.

Satisfaction in both segments is measured across seven core dimensions: trust; price for coverage; people; digital channels; problem resolution; product/coverage offering; and ease of doing business.

“The average shopping rate among home insurance customers has climbed to a record high of 6.8 percent through the second quarter of 2024, up from 5.9 percent two years ago,” said Breanne Armstrong, director of insurance intelligence at J.D. Power. “Many shoppers have ended up staying put because there are so few alternatives available, but carriers need to recognize that steady rate increases put policy retention at risk and has a negative effect on customer satisfaction.”

The study, based on responses from 14,122 homeowners and renters via online interviews conducted between November 2023 through July 2024, found that rising prices led consumers to shop around.

Among home insurance customers who receive an insurer-initiated rate increase, 37 percent are likely to shop for a new policy. The top reason given among those actively shopping new home insurance carriers is high rates.

Overall satisfaction among customers who receive an insurer-initiated rate increase is 594 (on a 1,000-point scale), 92 points lower than among those who did not receive an insurer-initiated rate increase.

Despite a record 6.8 percent of all home insurance customers actively shopping for new polices, just 2.2 percent of homeowners switched policies as a result, down from 2.5 percent two years ago.

Bundling home and auto policies has declined significantly in 2024 compared with 2023, but there is growing intent to switch auto insurance without switching home insurance. Specifically, 21 percent of customers say they “definitely will” also switch their home insurance if they switch their auto insurance, which is down from 24 percent a year ago.

The survey found the likelihood that home insurance customers will shop for a new policy following an insurer-initiated rate increase can be mitigated by clear communication with their insurer.

Among customers who receive an insurer-initiated rate increase, those who completely understand the reason for the increase are 14 percentage points less likely to shop for a new policy than those who do not understand the reason for the rate increase.

Customers who completely understand the reason for the rate increase are also 21 percentage points more likely to strongly agree that their insurer puts the interests of its customers first.

How Insurers Rank

Chubb ranks highest in the homeowners insurance segment, with a score of 688. AIG (680) ranks second and Amica (679) ranks third.

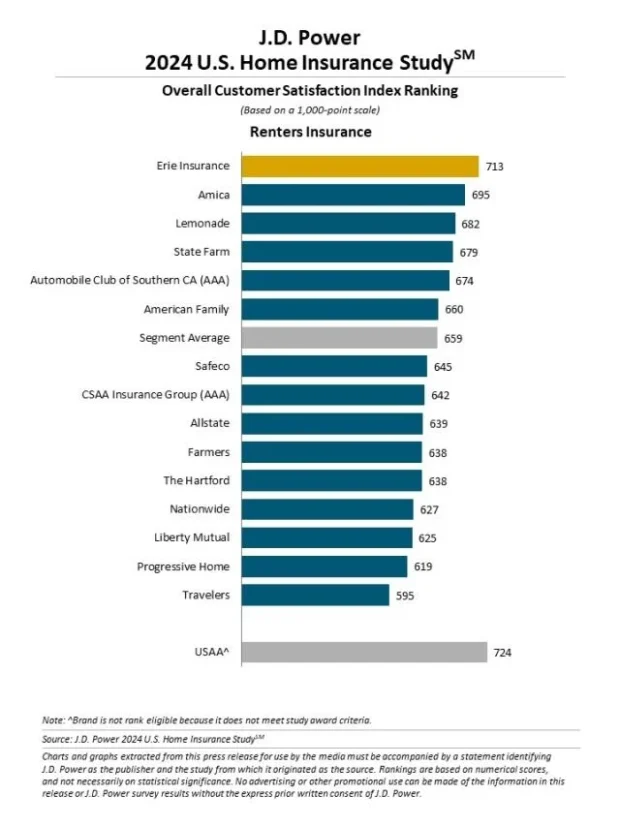

Erie Insurance ranks highest in the renters insurance segment for a second consecutive year, with a score of 713. Amica (695) ranks second and Lemonade (682) ranks third.

For more information about the U.S. Home Insurance Study, visit https://www.jdpower.com/business/insurance/us-home-insurance-study.

RLI Inks 30th Straight Full-Year Underwriting Profit

RLI Inks 30th Straight Full-Year Underwriting Profit  What Analysts Are Saying About the 2026 P/C Insurance Market

What Analysts Are Saying About the 2026 P/C Insurance Market  Nearly 26.2M Workers Are Expected to Miss Work on Super Bowl Monday

Nearly 26.2M Workers Are Expected to Miss Work on Super Bowl Monday