According to industry rating agency AM Best, there are enough positive factors to give the cyber insurance market a ‘stable’ outlook despite a stall in premium growth.

Analysts at AM Best issued a segment outlook and report Monday, and said the cyber market in 2023 was essentially flat following a tripling of the market’s premium growth from 2019-2022.

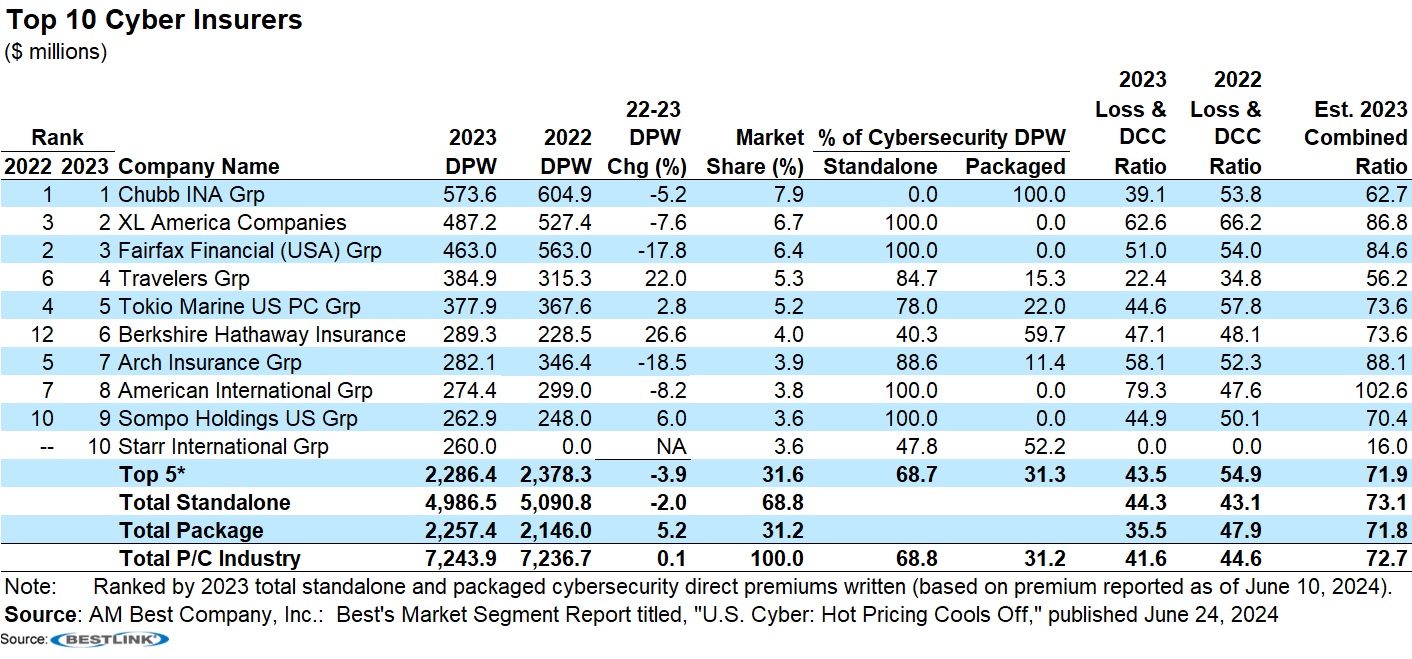

Still, some insurers recorded double-digit growth in direct premiums written for cyber last year, including Berkshire Hathaway Insurance and Starr International Group, which vaulted onto a list of top 10 cyber insurers compiled by AM Best analysts.

(Editor’s Note: Earlier this year, during a Berkshire Hathaway annual meeting, Vice Chair Ajit Jain reported that he tells professionals in Berkshire’s insurance operations to avoid writing cyber insurance when they can. Related article: Berkshire Wary of “Fashionable’ Cyber Insurance, AI)

Referring to the industrywide figures, Christopher Graham, senior industry analyst at AM Best, said, “The reduction in rates has been due to various factors, including increased competition from the supply side.”

“In addition, improving cybersecurity practices and decreases in claims frequency have also led to rate reductions after a period of accelerated rate increases driven by a surge in ransomware attacks in 2020 and 2021,” he said.

AM Best’s comments on market growth were based on filings from the National Association of Insurance Commissioners, but the agency believes a good amount of premium comes from non-NAIC filers like captives and Lloyd’s.

Surplus lines carriers in 2022 accounted for a majority of the cyber market and expanded market share in 2023, said AM Best, who believes this market in particular will continue to grow since these insurers can respond quickly to insureds’ needs, especially for small- and medium-sized enterprises—a customer base AM Best expects to grow as these business move to digital platforms.

“We expect that cyber coverage will continue to grow over time, as the heightening awareness of cyber risks contributes to an increase in exposures and, correspondingly, an increase in demand for cyber insurance,” Fred Eslami, associate director, said.

Cyber insurers rely heavily on reinsurance, with over 50 percent of premiums ceded to reinsurers with sufficient capacity. If reinsurers were to pull back in any way to limit their exposure, the primary market could change its appetite for cyber insurance.

In recent years, insurers and reinsurers put increasingly stringent underwriting standards in place, such as exclusions for cyber war and silent cyber. Still, systemic risk has become more of a concern for the cyber insurance marketplace, and models have yet to adequately be tested, AM Best said.

As for the ranking of carriers writing cyber in the U.S., Chubb is the largest, with 100 percent of direct premiums from packaged products. XL America and Fairfax Financial are next, with 100 percent of DPW in standalone coverage.

Travelers moved up two places in the ranking, having increased DPW 22 percent in 2023 compared to 2022. Berkshire Hathaway’s 26.6 percent jump propelled the group up six spots—from 12th to 6th on AM Best’s listing.

The AM Best listing shows Starr with no cyber premiums reported in 2022 but $260 million in 2023, giving it a 10th place ranking.

A version of this article was previously published on the Insurance Journal website. Reporter Chad Hemenway is the National Editor of Insurance Journal.

Earnings Wrap: With AI-First Mindset, ‘Sky Is the Limit’ at The Hartford

Earnings Wrap: With AI-First Mindset, ‘Sky Is the Limit’ at The Hartford  RLI Inks 30th Straight Full-Year Underwriting Profit

RLI Inks 30th Straight Full-Year Underwriting Profit  How Americans Are Using AI at Work: Gallup Poll

How Americans Are Using AI at Work: Gallup Poll  Earnings Wrap-Up: AXIS Expanding Insurance Biz, Shrinking Re Book

Earnings Wrap-Up: AXIS Expanding Insurance Biz, Shrinking Re Book