The wave of technological advancements generating, storing and using data has spurred on InsurTechs interested in revolutionizing insurance businesses, including those dedicated to commercial auto insurance.

Executive Summary

PART 3 of THREE-PART ARTICLE. After a tumultuous decade for the U.S. commercial auto insurance industry, fleet managers and insurance providers are rethinking how road experience should be monitored, underwritten and priced with the help of accelerating technological advancements. Many of these advancements aim to directly improve road safety, and others are expanding the insurance toolbox used to segment risk.

In this three-part article, a consulting actuary from Milliman and executives from Luminant Analytics and meshVI describe how advancements in data and tech are revamping the commercial auto insurance industry.

Part 1 provides an overview of the U.S. commercial auto insurance line’s historical performance and key drivers of the current market performance.

Part 2 details the vast improvements in technology and data that the industry has embraced in the last decade.

Part 3 focuses on the growth and positive performance of a recent cohort of commercial auto InsurTech startups in the last five years.

When the InsurTech investments landed, a popular vehicle was the MGA. Because of their size, MGAs are less burdened by technological legacies and can experiment more effectively with new products and underwriting practices than incumbents. Commercial auto was no exception.

Three well-known examples are HDVI, Nirvana and Cover Whale. Each has unique models that incorporate telematics data into risk selection, pricing and risk management. In addition to the data, they are also leveraging advanced technology, like computer vision, into their models.

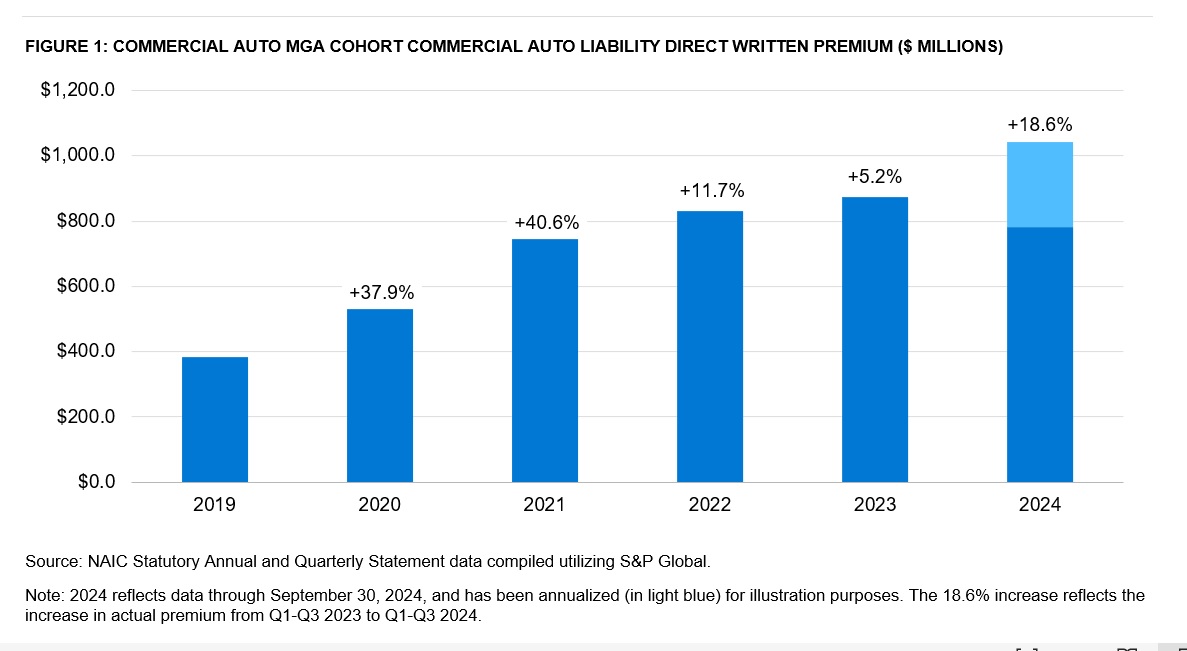

The popularity and rapid growth of MGAs also became apparent in the insurance data as the commercial auto liability written premium for well-known MGA-fronting companies grew at a rapid pace between 2019 and 2022, as shown in Figure 1, with the cohort of companies shown on pace for $1 billion in annual premium in 2024. A large portion of the recent premium growth was driven by new MGA entrants to the market and increased writings for established MGA players. Eventually, adverse experience across the commercial auto industry also contributed to increased premium through rate increases on existing business.

The InsurTech activities in the initial phase have been termed as “InsurTech 1.0,” where outside talent with no domain expertise was considered necessary for disruption, and unqualified growth was the need of the hour—mainly in direct-to-consumer personal lines ventures. This phase of startups attracted notable venture capital investment, and McKinsey & Company suggested that this “created significant pressure on InsurTechs to scale—and to do so quickly.”

Some insurance companies also opened their doors to this growth and established programs to front and partner with the emerging MGAs, with commercial lines coming into the mix. Several InsurTech startups formed from 2018-2021 have since gone out of business making funding for upcoming startups harder as investors tightened their wallets and insurance companies became more selective in which MGAs to partner with. The struggles of these early InsurTechs are widely documented. (See “Related Content” sidebar).

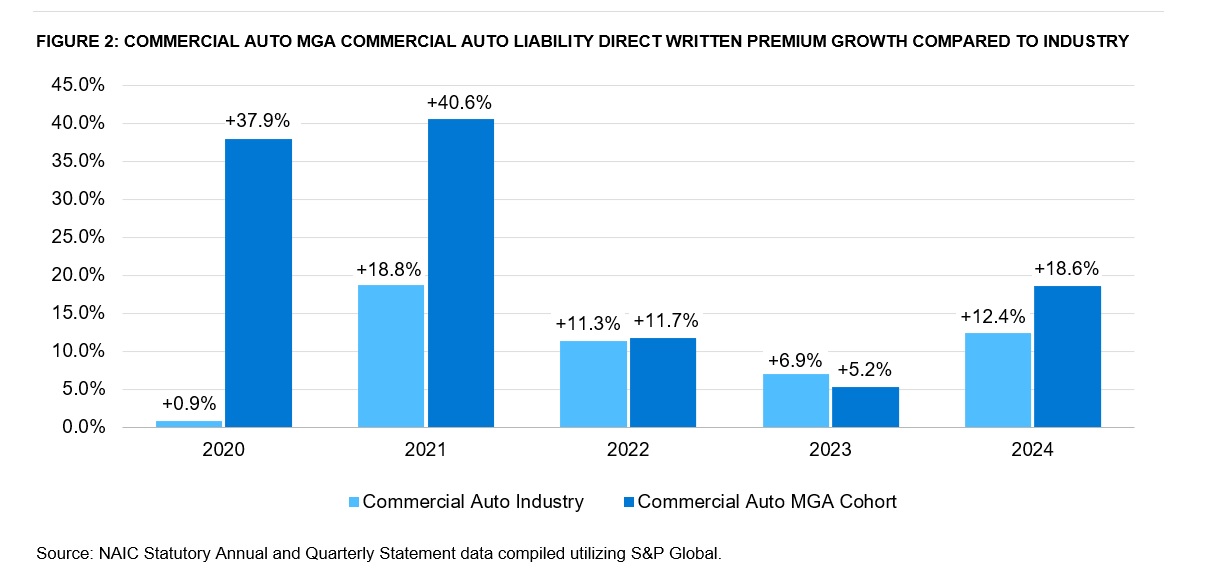

Figure 2 shows this rapid premium growth and MGA adoption relative to the premium increases observed by the commercial auto industry as a whole in 2020 and 2021. This was followed by a period of reduced MGA growth in 2022, a time when InsurTech funding generally, across the P/C segment and the insurance industry overall, started to plummet. Eventually, the exit of prominent MGAs and increased selectiveness of fronting carriers offset any MGA growth, resulting in lower relative premium growth compared to the commercial auto industry in 2023.

Looking Ahead to InsurTech 2.0 for Commercial Lines

The trials of InsurTech 1.0 eventually led to the birth of InsurTech 2.0, where responsible underwriting delivered through local channels and agents, and risk capacity delivered through strategic partnerships, started gaining traction. The first wave of InsurTechs, InsurTech 1.0, learned the hard way that the insurance industry is not easily disrupted, as investors pulled funds from insurance ventures due to differing expectations. The current investment focus is on more sustainable, less flamboyant Silicon Valley sorts of startups, with well-identified markets and a sharp eye on profitability—nurturing the notion that growth cannot happen at all costs.

The newer wave of startups has since focused on collaboration rather than disruption—smart risk-taking that combines insurance expertise with advanced data and technology. The explosion of generative AI (GenAI) has put further pressure on insurers to deliver the benefits of technology to consumers, and traditional market players have evolved to place greater emphasis on innovation, fueling synergies between the InsurTech startups and incumbents. InsurTech 2.0 combines the demand for technology with vetted innovation vehicles.

This more selective group of MGAs saw notable premium growth in 2022 and 2023, but it is not apparent in Figure 2, as the impact from InsurTech 1.0 exits had a large effect on the market’s overall written premium. The emergence and expansion of InsurTech 2.0 players suggests that the year-over-year premium growth of MGAs in the coming years may be higher than the overall commercial auto industry once again, signifying the start of this new MGA era.

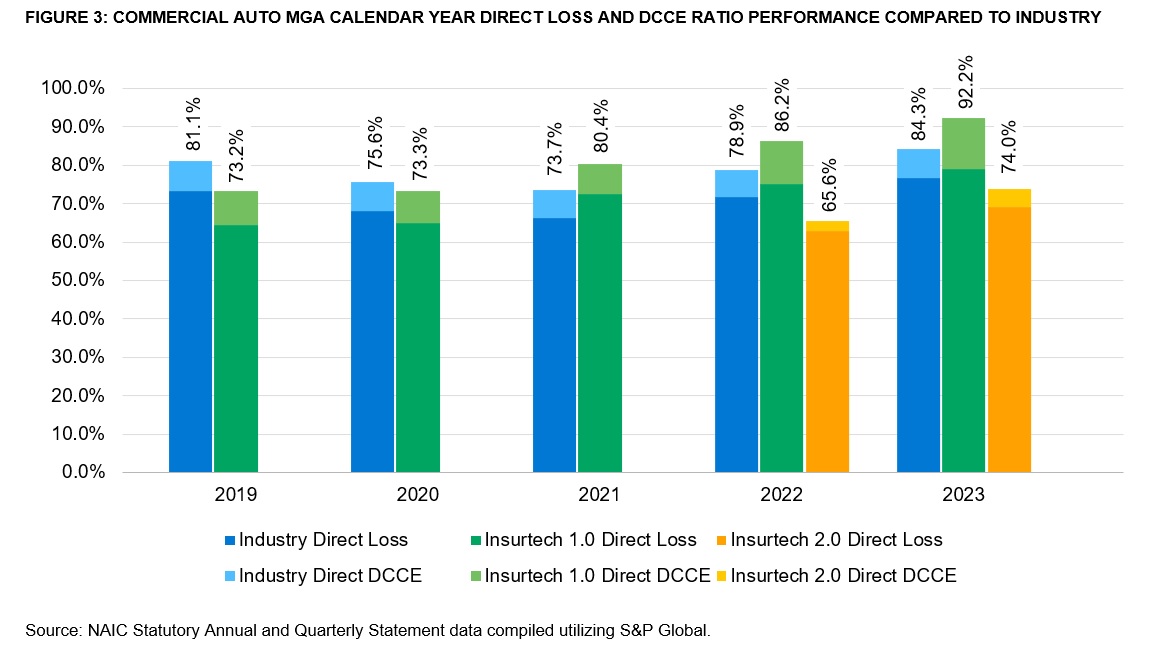

The performance of InsurTech 1.0 in commercial auto initially looked promising but eventually deteriorated to a level that has been more adverse than the overall commercial auto industry (as shown in Figure 3). Some of this was certainly due to unsustainable growth goals, but there were other factors at play. In many instances, MGAs have aimed to serve the needs of a market segment that is underserved or not as well understood by the industry. Examples of this are MGAs focused exclusively on long-haul trucking, a segment especially susceptible to nuclear verdicts, or rideshare, a rapidly evolving segment.

Beyond insuring potentially riskier business, these MGAs have seen higher expenses, as illustrated by the higher defense and cost containment expenses (DCCE) in recent years.

The InsurTech 1.0 cohort in Figure 3 primarily contains insurers that provide fronting services to multiple MGAs and have done so for the past five years or more. The InsurTech 2.0 cohort contains the insurers that tend to focus on fronting a single technology-focused MGA and that have looked to more cautiously address the issues in the market. Many of the InsurTech 2.0 companies have previously been mentioned by name in this three-part article. (See, for example, Part 2, “Better Results Ahead? Technology Improvements in Commercial Fleets“)

Figure 3 shows that InsurTech 2.0 performance has been promising in the last two years, with loss experience below the industry level along with impressively low expense ratios. This suggests that the technological focus and implementation of telematics solutions may be finally leading to lower losses and better claims-handling efficiencies. However, it’s still too early to draw definitive conclusions, as this cohort has relatively low premium volume compared to the overall industry. It is also unclear how this experience will develop over time, given that the commercial auto industry has observed some years where the accident year loss ratio has increased nearly 10 percentage points in the span of five years, as illustrated by accident year 2019 in Figure 2 in the first part of this article series, “Performance Review: Why Insurers Struggle to Underwrite, Price and Reserve for Commercial Auto Risks.”

The full impact of advanced technology remains to be seen, but current performance is a positive indication that the second wave of MGAs may be doing a better job at curbing the adverse commercial auto experience. While many of the InsurTech 2.0 companies are still in early stages, some of the more mature players are beginning to attract the interest of industry investors again; in February, HDVI secured $40 million in growth capital, while a month later Nirvana raised $80 million in funding based on a valuation of $830 million.

The landscape of InsurTech 2.0 extends beyond MGAs to include a diverse array of companies, including software as a service (SaaS) providers and retail agencies. OpenEyes, for example, which launched in 2023 as a retail agency InsurTech, leverages computer vision and AI to sharpen underwriting, streamline claims handling, and enable fleet managers and safety officers to identify the sources of risk in their fleet, empowering them to implement practices to reduce losses—ultimately leading to better insurance pricing. Similarly, LogRock expanded to include retail agency operations in 2024, combining compliance software and driver recruiting tool for its insurance clients.

Other examples of SaaS transportation InsurTechs include companies focused on policy administration, agency management, fleet management, driver compliance, claims management, insurance distribution and risk management. While these types of InsurTechs don’t directly write insurance, their impact on the industry steadily gains significance as the industry continues to evolve.

Looking Ahead

Commercial auto in general, and trucking in particular, is the lifeblood of America’s day-to-day activities. A rough patch of adverse performance has led many incumbents to exit, but the vast size of the line of business—around $64 billion in gross written premium for 2023 according to NAIC figures—is too large for carriers to simply ignore.

Additionally, the upcoming (semi-) autonomous trucking wave renders the industry vulnerable to the dislocation of its services by the truck and part makers, so ignoring the opportunity for improvements is perilous.

As the evolving numbers show from InsurTech 2.0, there is still hope—and a whole-hearted, mission-driven adoption of data and technology as the only answers to a longer-term financial equilibrium for commercial auto insurance.

This article is part of a three-part series of articles describing how advancements in data and tech are revamping the commercial auto insurance industry.

In Part 1, the authors provided a historical view of commercial auto insurance industry loss over the last decade-and-a-half, and unfavorable loss development patterns for recent accident years.

In Parts 2 and 3, they described the vast improvements in technology and data that the fleet management and commercial auto insurance industries have embraced in the last decade, and the growth and positive performance of a recent cohort of commercial auto startups in the last five years.

Note: The authors have provided consulting services to some companies mentioned in this article. The statements made within should not be viewed as specific endorsements and are based on publicly available information.

Allianz Built an AI Agent to Train Claims Professionals in Virtual Reality

Allianz Built an AI Agent to Train Claims Professionals in Virtual Reality  Execs, Risk Experts on Edge: Geopolitical Risks Top ‘Turbulent’ Outlook

Execs, Risk Experts on Edge: Geopolitical Risks Top ‘Turbulent’ Outlook  Berkshire-owned Utility Urges Oregon Appeals Court to Limit Wildfire Damages

Berkshire-owned Utility Urges Oregon Appeals Court to Limit Wildfire Damages  Preparing for an AI Native Future

Preparing for an AI Native Future