The wave of technological advancements generating, storing and using data has spurred on InsurTechs interested in revolutionizing insurance businesses, including those dedicated to commercial auto insurance.

Executive Summary

PART 3 of THREE-PART ARTICLE. After a tumultuous decade for the U.S. commercial auto insurance industry, fleet managers and insurance providers are rethinking how road experience should be monitored, underwritten and priced with the help of accelerating technological advancements. Many of these advancements aim to directly improve road safety, and others are expanding the insurance toolbox used to segment risk.

In this three-part article, a consulting actuary from Milliman and executives from Luminant Analytics and meshVI describe how advancements in data and tech are revamping the commercial auto insurance industry.

Part 1 provides an overview of the U.S. commercial auto insurance line's historical performance and key drivers of the current market performance.

Part 2 details the vast improvements in technology and data that the industry has embraced in the last decade.

Part 3 focuses on the growth and positive performance of a recent cohort of commercial auto InsurTech startups in the last five years.

When the InsurTech investments landed, a popular vehicle was the MGA. Because of their size, MGAs are less burdened by technological legacies and can experiment more effectively with new products and underwriting practices than incumbents. Commercial auto was no exception.

Three well-known examples are HDVI, Nirvana and Cover Whale. Each has unique models that incorporate telematics data into risk selection, pricing and risk management. In addition to the data, they are also leveraging advanced technology, like computer vision, into their models.

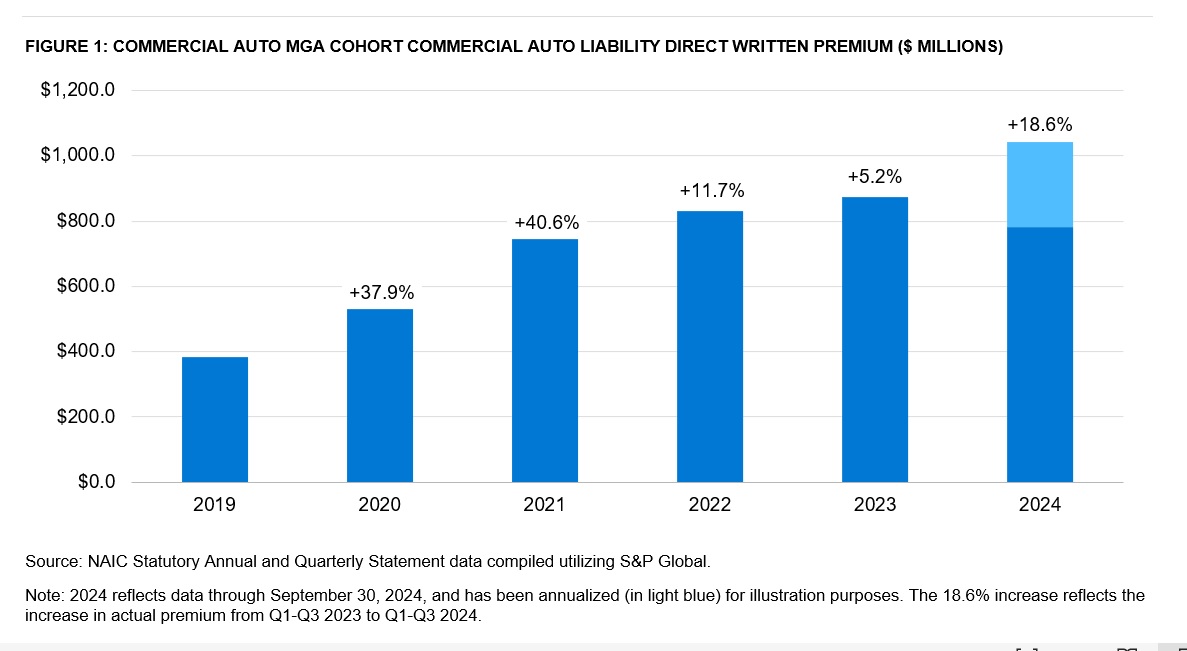

The popularity and rapid growth of MGAs also became apparent in the insurance data as the commercial auto liability written premium for well-known MGA-fronting companies grew at a rapid pace between 2019 and 2022, as shown in Figure 1, with the cohort of companies shown on pace for $1 billion in annual premium in 2024. A large portion of the recent premium growth was driven by new MGA entrants to the market and increased writings for established MGA players. Eventually, adverse experience across the commercial auto industry also contributed to increased premium through rate increases on existing business.

The InsurTech activities in the initial phase have been termed as “InsurTech 1.0,” where outside talent with no domain expertise was considered necessary for disruption, and unqualified growth was the need of the hour—mainly in direct-to-consumer personal lines ventures. This phase of startups attracted notable venture capital investment, and McKinsey & Company suggested that this “created significant pressure on InsurTechs to scale—and to do so quickly.”

{kind=link}