Commercial auto insurance has experienced poor performance in aggregate, but the industry has also seen pockets of improvement resulting from considerable and unique technological advancements.

Executive Summary

PART 2 of THREE-PART ARTICLE. After a tumultuous decade for the U.S. commercial auto insurance industry, fleet managers and insurance providers are rethinking how road experience should be monitored, underwritten and priced with the help of accelerating technological advancements. Many of these advancements aim to directly improve road safety, and others are expanding the insurance toolbox used to segment risk.

In this three-part article, a consulting actuary from Milliman and executives from Luminant Analytics and meshVI describe how advancements in data and tech are revamping the commercial auto insurance industry.

Part 1 provides an overview of the U.S. commercial auto insurance line’s historical performance and key drivers of the current market performance.

Part 2 details the vast improvements in technology and data that the industry has embraced in the last decade.

Part 3 focuses on the growth and positive performance of a recent cohort of commercial auto InsurTech startups in the last five years.

The primary drivers behind these advancements have come from commercial vehicle owners and fleet managers adhering to changes in safety improvements, environmental sustainability and government regulations as well as an underlying push for operational efficiencies.

While different in their purposes, many of these changes have and will impact risk profiles, claims frequency and severity, and insurance products.

Regulatory demands often largely influence technological advancement and implementation. Examples in two key areas include mandatory compliance with existing regulations, such as implementation of electronic logging devices (ELDs), and the anticipated forthcoming regulations concerning autonomous vehicles.

Telematics and ADAS

Technology improvements focused on safety include systems like advanced driver assistance systems (ADAS), which are increasingly prevalent in commercial vehicles. Likewise, telematics devices can include operational efficiencies, compliance and safety advancements. Telematics devices range from front-facing, driver-facing and side cameras to real-time vehicle tracking, geospatial monitoring, remote diagnostics, predictive maintenance, driver behavior monitoring, route optimization and fuel efficiency tracking.

Related article: Performance Review: Why Insurers Struggle to Underwrite, Price and Reserve for Commercial Auto Risks

The advancement in telematics provides not only an immediately obvious solution but also invaluable data that the insurance industry is beginning to leverage. One of the main obstacles the insurance industry faces in fully utilizing this revolutionary data is the vast number of telematics service providers (TSPs) and their unique data and technological capabilities.

The insurance industry employs several strategies to access and leverage telematics data. Nirvana and HDVI, managing general agencies, have adopted a strategy of requiring their insured clients to use specific telematics vendors with which they’ve established partnerships. Some established insurance companies, like Progressive’s Smart Haul program, have opted to build their own connections and offer premium discounts to customers who work with preferred vendors.

A new category of technology vendors has emerged, specializing in aggregating and normalizing data from multiple TSPs. These companies act as intermediaries, simplifying the data collection and analysis process. TruckerCloud, for example, has successfully integrated with over 40 telematics vendors, effectively covering approximately 95 percent of commercial transportation TSPs. On top of the data aggregation, other technology solutions provide risk scoring that works with any TSP. Milliman’s AccuRate Fleet Score,for example, allows insurers to utilize the telematics data for underwriting and pricing without being tied to specific TSPs. (Editor’s Note: One of the authors of this article is a consultant at Milliman.)

Artificial Intelligence

Artificial intelligence (AI) is also being leveraged in telematics to improve safety, especially in computer vision built into cameras and advanced behavior analytics. The advanced camera systems with computer vision can monitor driver behavior in real time, detect potential hazards on the road, and identify signs of driver fatigue or distraction.

Several companies promote their use of this AI-driven telematics advancement, including Netradyne, Nauto, LightMetrics, Motive and Samsara. These companies aim to improve safety, efficiency and compliance through their advanced driver monitoring and external vehicle-surrounding analyses. In some cases, AI-enhanced telematics devices also provide complex behavior analytics, leading to deeper insights into driving patterns and vehicle performance.

In addition to telematics usage, fleets are deploying AI in conjunction with electrification and alternative fuels for sustainability, which reduce overall operating costs. AI and machine learning are also gaining traction for predictive analytics around maintenance, risk management, route optimization and demand forecasting. Once more broadly adopted, this data will provide valuable insights that should be leveraged by the insurance industry.

Smart Devices and Integrations

The industry is developing and adopting technologies for a more connected, autonomous and sustainable environment. These technologies include advanced infotainment and user interfaces; large, high-resolution displays; seamless integrations with smart devices; voice-activated controls; and AI assistants. While still emerging, the insurance industry will be tracking the implications of how the implementation of these systems impacts the overall risk.

With the new technological developments emerging, it’s important to note that adoption varies significantly within the broad spectrum of commercial auto segments. Fleet size, age of the fleet, original equipment manufacturer (OEM) versus after-market, and operation types like last mile, long-haul or freight versus passenger carriers are some of the many factors that affect adoption as well as availability of current and future technologies. Overall, as an industry, much progress has been made and many new advancements are on the horizon.

Data Usage in Commercial Auto Insurance

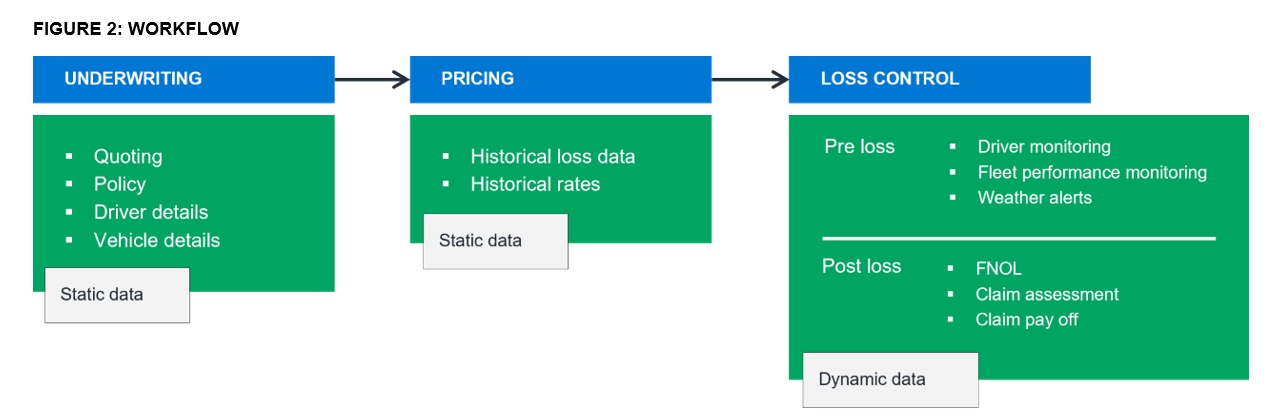

Carriers have incorporated the new sources of data from these technology advances into the entire value chain of writing an auto policy—from underwriting to pricing and loss control.

Data is delivered to the value chain through various delivery mechanisms, and some commonly used terminology is explained below.

Dynamic data. This refers to real-time data generated through devices placed within or outside of the vehicle. Ownership of this data varies and may be owned by the fleet, insurer or a third party.

Telematics is a broad category used to describe systems that monitor the performance of trucks and cars using GPS and onboard diagnostics (OBD), including sensors. The metrics measured are usually motion: speed and idling, braking, fuel use, tire pressure, and engine data.

As described previously, popular telematic integrations are dash cameras, ELDs and weather alerts. ELDs are used to automatically record driving time and hours of service (HOS). The integrations can be used to highlight driver metrics in real time, though the real-time tracking of commercial motor vehicles is not required in the ELD rule, a set of requirements governing the collection and retention of motor carrier data, which came into effect on Dec. 16, 2019.

Dash cameras are used to capture driver movements and reactions, and some technology is augmented through AI to coach driver behavior. The resulting data can be brought into a cloud management software application for use by fleets and insurance carriers.

Static data. This refers to data that is not real-time, mostly available from public records. While not real-time, the data is not truly “static” as it is updated over time, albeit subject to reporting lag.

This data spans vehicle characteristics such as vehicle identification number (VIN), driver characteristics (license and previous accident record history) and road characteristics (accident spots, road structure). Most of the county-level data is available from various “open” sources. This data also commonly includes U.S. Department of Transportation (DOT) inspection data captured by the FMCSA for commercial vehicles.

Third-party vendors aggregate these data sources using their own proprietary sources and make them available to insurers for analytical and pricing uses, and to retailers and wholesalers to vet and appropriately market to clients.

When we look at how these data sources can be used in a commercial auto policy, the workflow looks like the illustration in Figure 2.

Despite technological advances in data generation and analytics, most U.S. rating plans for commercial auto still rely on historical static data for making underwriting and pricing decisions. However, insurers are moving toward incorporating dynamic pricing by using real-time user behavior, especially when it comes to usage-based insurance (UBI).

Supply vs. Demand of Third-Party Data for Commercial Auto

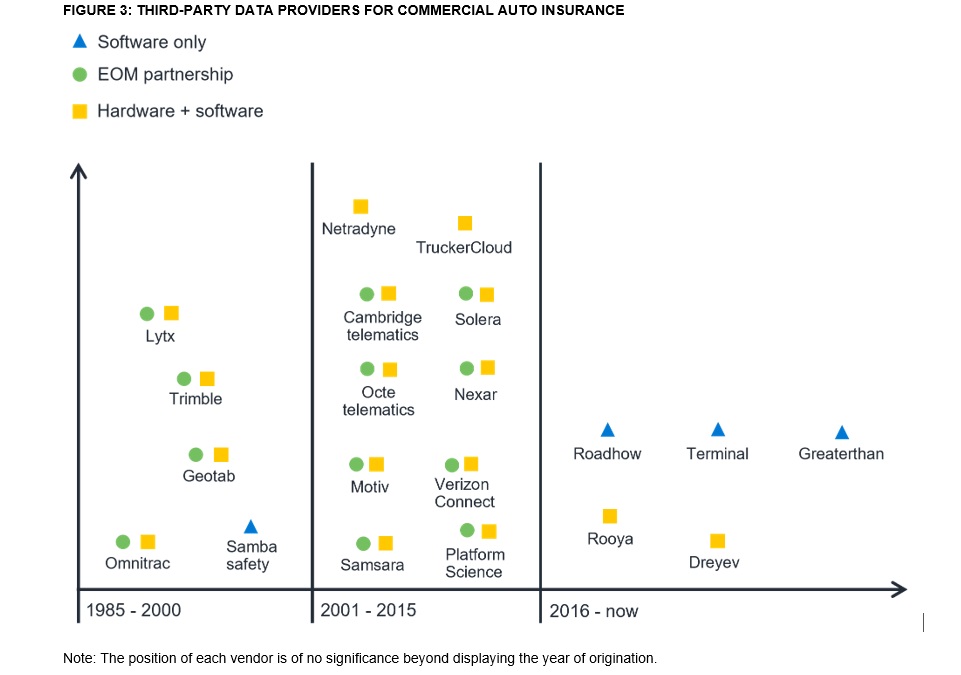

The use of these different sources of data helps the industry to proactively assess trends, rather than reactively adjusting pricing after compiling enough historical claims data. However, it has been a shower of plenty when it comes to data providers in the last decade-and-a-half. The graph in Figure 3 is a simplified view of what the data-offering landscape looks like for commercial auto.

Many of the early data providers offered a full-stack approach to offering data to insurers by partnering with OEMs to offer both hardware and software. The aforementioned data aggregators are addressing the lack of fully integrated data streams in the insurance industry today. Figure 3 does not depict full-stack insurers that use their own telematics platforms.

Despite the options, commercial auto insurers have been reluctant to adopt new data sources. According to a survey done by Samba Safety and the National Alliance for Insurance Education and Research in 2023 of around 335 P/C commercial line participants, about 38 percent of commercial line carriers are in the early stages of usage, but only 27 percent of commercial auto respondents have internal, dedicated telematics or connected car teams at their organizations, and only 6.25 percent have robust infrastructures to handle large volumes of telematics data.

Related article: Study: Most Commercial Auto Insurance Businesses Researching Telematics.

The study also revealed that for nearly 40 percent of commercial auto insurers polled, UBI is not part of their current business plan.

What is interesting is that, despite being highly regulated, personal auto carriers have been way ahead of commercial auto carriers in integrating newer, richer data sources into their everyday business decisions. Personal auto policy data collection processes have a history of being more detail-oriented and thorough, right from policy inceptionn, than commercial auto. This can explain why personal auto has a head start here. Additional challenges of data privacy concerns, distrust of data sources and lack of data-related infrastructure add to the hesitancy for commercial carriers to adopt the technology at the same rate as personal lines carriers.

***

This article is part of a three-part series of articles describing how advancements in data and tech are revamping the commercial auto insurance industry.

In Part 1, the authors provided a historical view of commercial auto insurance industry loss over the last decade and a half, and unfavorable loss development patterns for recent accident years.

In Part 3, they will review the growth and positive performance of a recent cohort of commercial auto startups, who are leaning into the vast improvements in technology and data described in the present article.

Note: The authors have provided consulting services to companies mentioned in this article. The statements made within should not be viewed as specific endorsements and are based on publicly available information.

How Americans Are Using AI at Work: Gallup Poll

How Americans Are Using AI at Work: Gallup Poll  Earnings Wrap-Up: AXIS Expanding Insurance Biz, Shrinking Re Book

Earnings Wrap-Up: AXIS Expanding Insurance Biz, Shrinking Re Book  Nearly 26.2M Workers Are Expected to Miss Work on Super Bowl Monday

Nearly 26.2M Workers Are Expected to Miss Work on Super Bowl Monday  Insurance Groundhogs Warming Up to Market Changes

Insurance Groundhogs Warming Up to Market Changes