It has been 11 years since commercial auto loss ratios have outperformed the greater property/casualty industry.

Executive Summary

PART 1 of THREE-PART ARTICLE. After a tumultuous decade for the U.S. commercial auto insurance industry, fleet managers and insurance providers are rethinking how road experience should be monitored, underwritten and priced with the help of accelerating technological advancements. Many of these advancements aim to directly improve road safety, and others are expanding the insurance toolbox used to segment risk.

In this three-part article, a consulting actuary from Milliman and executives from Luminant Analytics and meshVI describe how advancements in data and tech are revamping the commercial auto insurance industry.

Part 1 provides an overview of the U.S. commercial auto insurance line’s historical performance and key drivers of the current market performance.

Part 2 details the vast improvements in technology and data that the industry has embraced in the last decade.

Part 3 focuses on the growth and positive performance of a recent cohort of commercial auto InsurTech startups in the last five years.

A lot has happened in that period—increasing capabilities for handheld devices, a global pandemic, the highest interest rates observed in decades—each of which impacted P/C insurance in unique ways. Despite numerous rate increases and more stringent underwriting, most commercial auto companies have struggled to improve performance as new drivers of losses continue to counteract improvements.

Commercial auto liability industry experience in 2024 is tracking similarly to 2023. At the time of this paper, only the first three quarters of data were available. Through Sept. 30, 2024, the commercial auto industry reported a 2024 calendar year loss ratio of 75.9 for commercial auto liability compared to a loss ratio of 76.6 in calendar year 2023. Meanwhile, the full P/C industry recorded a loss ratio of 62.4 in the first nine months of 2024 compared to 65.4 in 2023; however, it is worth noting that the 2024 data does not capture the impact of storms like Helene and Milton occurring in late September and early October.

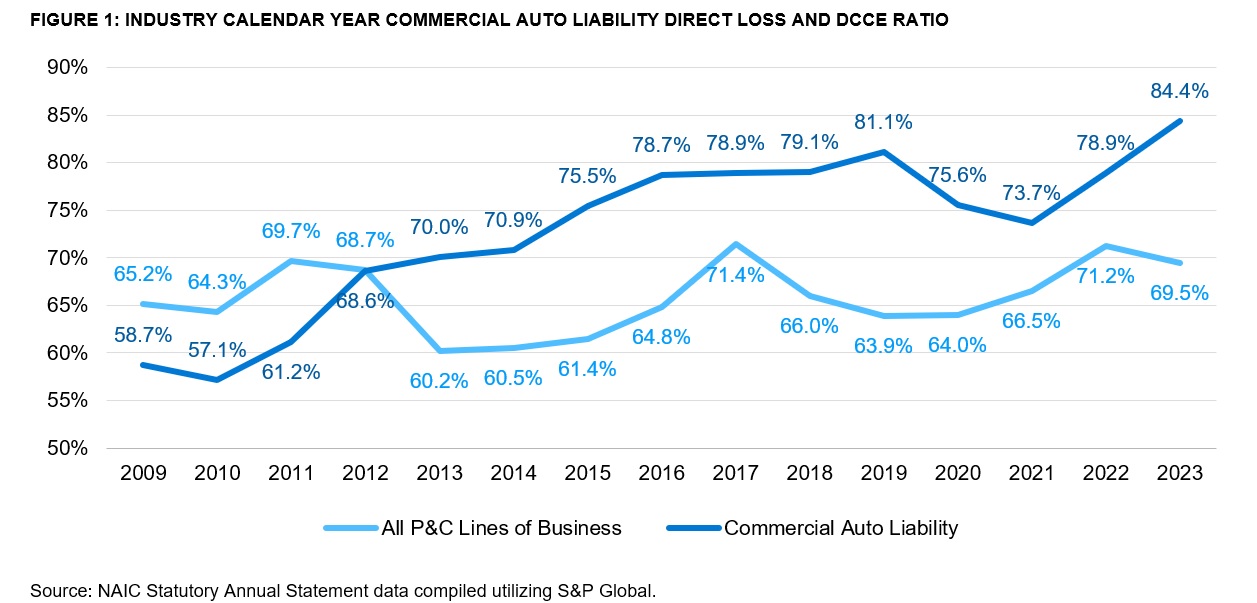

Note that these loss ratios exclude defense and cost containment expenses (DCCE) as this information was not compiled midyear, while the full-year figures in the graph below do include DCCE.

In 2023, the latest full-year data available that does include DCCE, the commercial auto liability loss ratio was 84.4—almost 15 points higher than the 69.5 loss ratio recorded for all P/C lines of business.

Commercial auto losses can be broadly classified by a number of factors, including macroeconomics, the litigation environment, driving behavior or some combination of the three. Insurers have varying degrees of control over each of these categories, so focusing efforts on areas that can be influenced is critical, especially when there are limited resources available to devote to each line of business.

Macroeconomic factors are outside of insurers’ control. Commercial auto physical damage has been especially impacted recently by the rising costs of replacement vehicles and vehicle repairs. Insurers can take steps to mitigate the influence of economic factors, such as expanding or shrinking business during certain points of the economic cycle or by better calibrating insurance trends that are linked to economic inflation. This is difficult to do proactively without credible data, so commercial auto insurers need to weigh the benefit of securing data to more effectively determine highly leveraged model assumptions like severity trend.

The litigation environment is also difficult to influence. The P/C insurance industry has struggled with the best way to handle social inflation, a broad term describing influences beyond economic factors that have led to an increase in insurance claims costs. The various causes of social inflation have been well researched and largely linked to shifts in the underlying litigation environment, yet it is difficult to precisely target the best ways to curb it. Commercial auto has been particularly impacted by social inflation as nuclear verdicts (i.e., high-dollar jury awards that far exceed expectations) have increased in recent years, leading to more attorney interest in commercial auto cases. A study by Milliman prepared for the American Property Casualty Insurance Association in 2022 found that the average cost of commercial auto claims with attorney representation jumped 21.3 percent over the five-year period from 2015-2019.

Related article: Data Points: Attorney Impact on Commercial Auto Losses

This impact is magnified even further as third-party litigation funding (TPLF) has provided the plaintiffs’ bar with more capital to litigate commercial auto claims.

Broader shifts in the litigation environment, such as TPLF and nuclear verdicts awarded by juries, can be addressed by tort reform, specifically requirements to disclose TPLF and caps on noneconomic damages. While some states have adopted measures along these lines, there are still jurisdictions that will continue to produce adverse outcomes for defendants.

Beyond pushing for tort reform, insurers can leverage data and technology to better understand the leading indicators of likely large settlements and properly allocate claims-handling resources to higher-risk cases.

Below the higher-level macroeconomic and social inflationary trends lies the basic driver of auto insurance losses: driver behavior. The developments in advanced driver assistance systems (ADAS) that are meant to improve road safety have been counteracted with an increase in driver distraction, due to handheld devices. (See, for example, “The State of Distracted Driving in 2023 & the Future of Road Safety,” Cambridge Mobile Telematics)

At face value, the use of mobile devices while driving may seem to be a bigger issue for personal vehicle operation, but various studies have shown that this also impacts commercial vehicle operation, notably a Federal Motor Carrier Safety Administration (FMCSA) study on distraction that found handheld interaction with cellphones increases the likelihood of collisions or unsafe road maneuvers, referred to as safety critical events in the study.

Insurers and fleet managers may not be physically in the vehicle with the driver, but advancing technology has increased the ability to monitor and train drivers to produce safer outcomes. This ranges from telematics that measure driving attributes like braking distance to enhanced visual monitoring that can remind a driver to keep their eyes on the road or put down their phone. A few of the innovative companies bringing variations of this technology into insurance are discussed in the second part of this three-part article, “Technology Improvements in Commercial Fleets.”

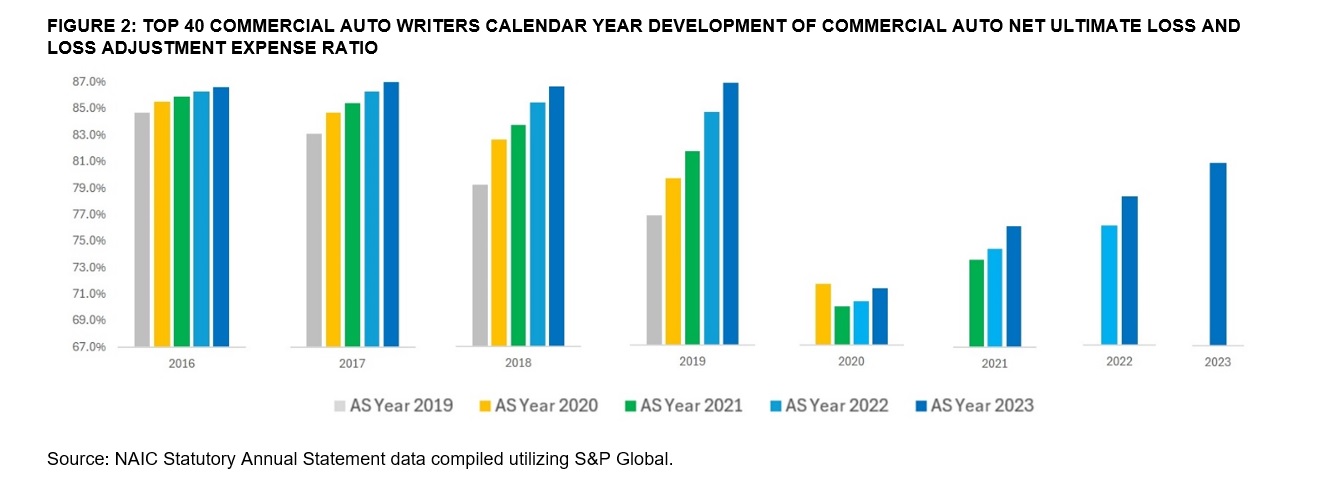

Together, economics, litigation and distracted driving are making it increasingly difficult to underwrite and price good commercial auto risks. And, equally or even more importantly, they have made it difficult to hold proper reserves for the potential liabilities. This is apparent in Figure 2, showing consistent upward development of most of the accident year 2016-2022 loss ratios at each successive calendar year-end. The upward development is evident for each accident year except for accident year 2020, which was heavily influenced by unusual driving patterns during the global pandemic.

Loss ratios have largely returned to pre-pandemic levels, but it remains to be seen whether the initial indications prove to be accurate or if loss ratios will continue to develop in the same manner that they did in the pre-pandemic years.

The consistent adverse development in subsequent calendar years further highlights the importance for commercial auto carriers to find leading indicators that are predictive of future trends.

More information on the state of the commercial auto market can be found in the 2023 Milliman Commercial Auto Liability Annual Report. (2023 Commercial Auto Liability Statutory Financial Results. Milliman Annual Report.)

In the second and third parts of this series of articles, we describe the vast improvements in technology and data that the fleet management and commercial auto insurance industries have embraced in the last decade, and the growth and positive performance of a recent cohort of commercial auto startups in the last five years.

Earnings Wrap: With AI-First Mindset, ‘Sky Is the Limit’ at The Hartford

Earnings Wrap: With AI-First Mindset, ‘Sky Is the Limit’ at The Hartford  Insurance Groundhogs Warming Up to Market Changes

Insurance Groundhogs Warming Up to Market Changes  What Analysts Are Saying About the 2026 P/C Insurance Market

What Analysts Are Saying About the 2026 P/C Insurance Market  Retired NASCAR Driver Greg Biffle Wasn’t Piloting Plane Before Deadly Crash

Retired NASCAR Driver Greg Biffle Wasn’t Piloting Plane Before Deadly Crash