Inadequate pricing for violations and accidents accounts for $4.7 billion in annual premium leakage for personal auto insurers.[1] Against a backdrop of ongoing riskier driving behaviors,[2] a new Verisk study reveals an unsettling storyline—but new data sources and innovations are enabling insurers to confront these challenges.

“As American roads have grown more deadly, [experts] blame…a breakdown in the social contract — the basic expectation that drivers will follow the rules…”

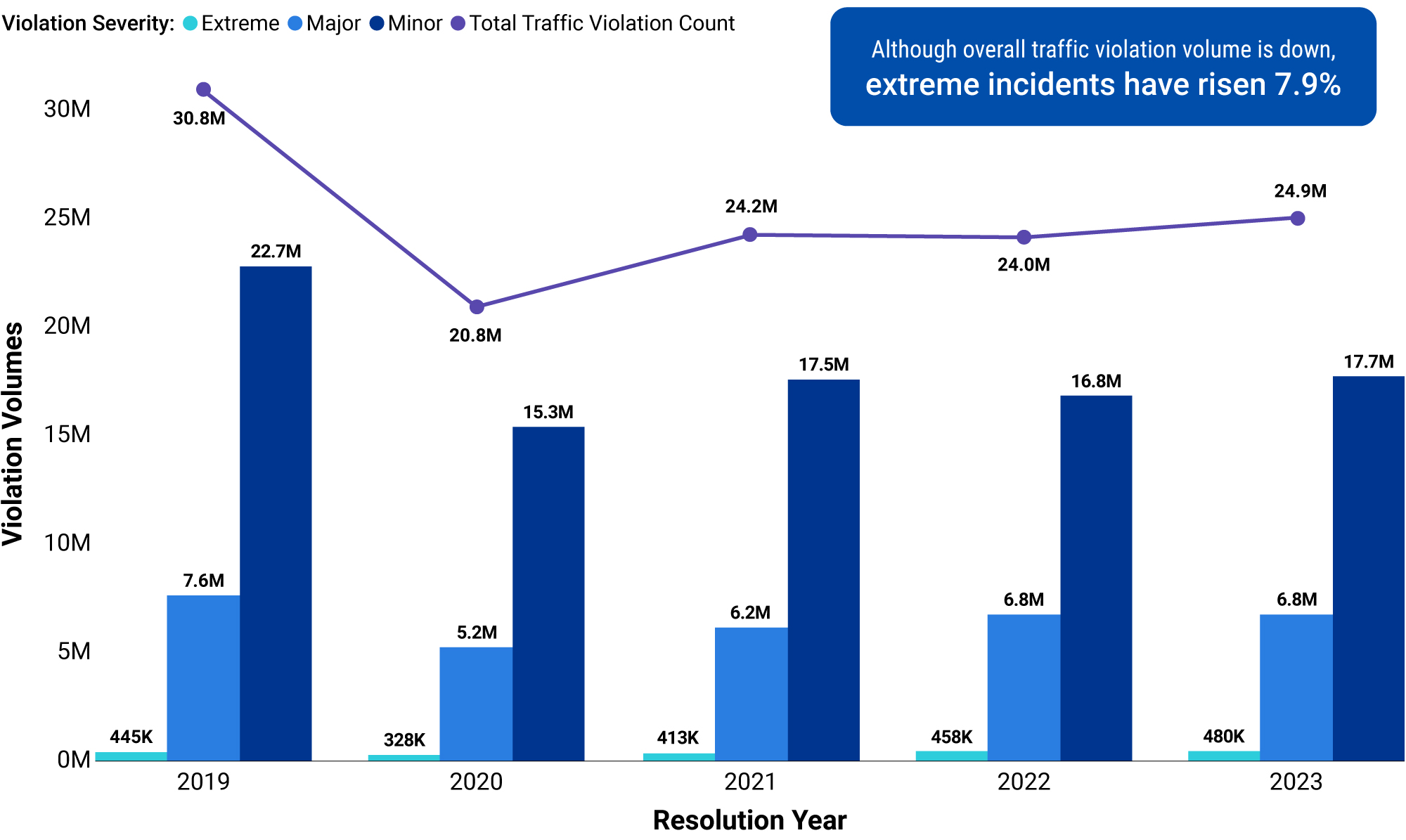

Extreme driving rises as surchargeable violation volume “evaporates”

A recent Verisk study finds police are issuing almost 20% fewer traffic violations compared with pre-pandemic levels, yet extreme incidents are up 7.9% over the same period—2023 versus 2019.[3]

Surchargeable violation volume is down 19.2% from 2019[3]

(Traffic incidents extrapolated to national totals)

The trend of police issuing fewer violations has had a large impact on insurers’ bottom lines. Beyond the profitability pressures for insurers, there is a fairness issue of safe drivers having to pay more than their share to cover the losses of riskier drivers—and the impacts to society in terms of lives lost and futures shattered.

“As American roads have grown more deadly, [experts] blame…a breakdown in the social contract—the basic expectation that drivers will follow the rules,” says an article in The New York Times that explores the complex reasons behind the dramatic drop-off in police enforcement of traffic violations.

Costs rise for traditional driving risk assessment

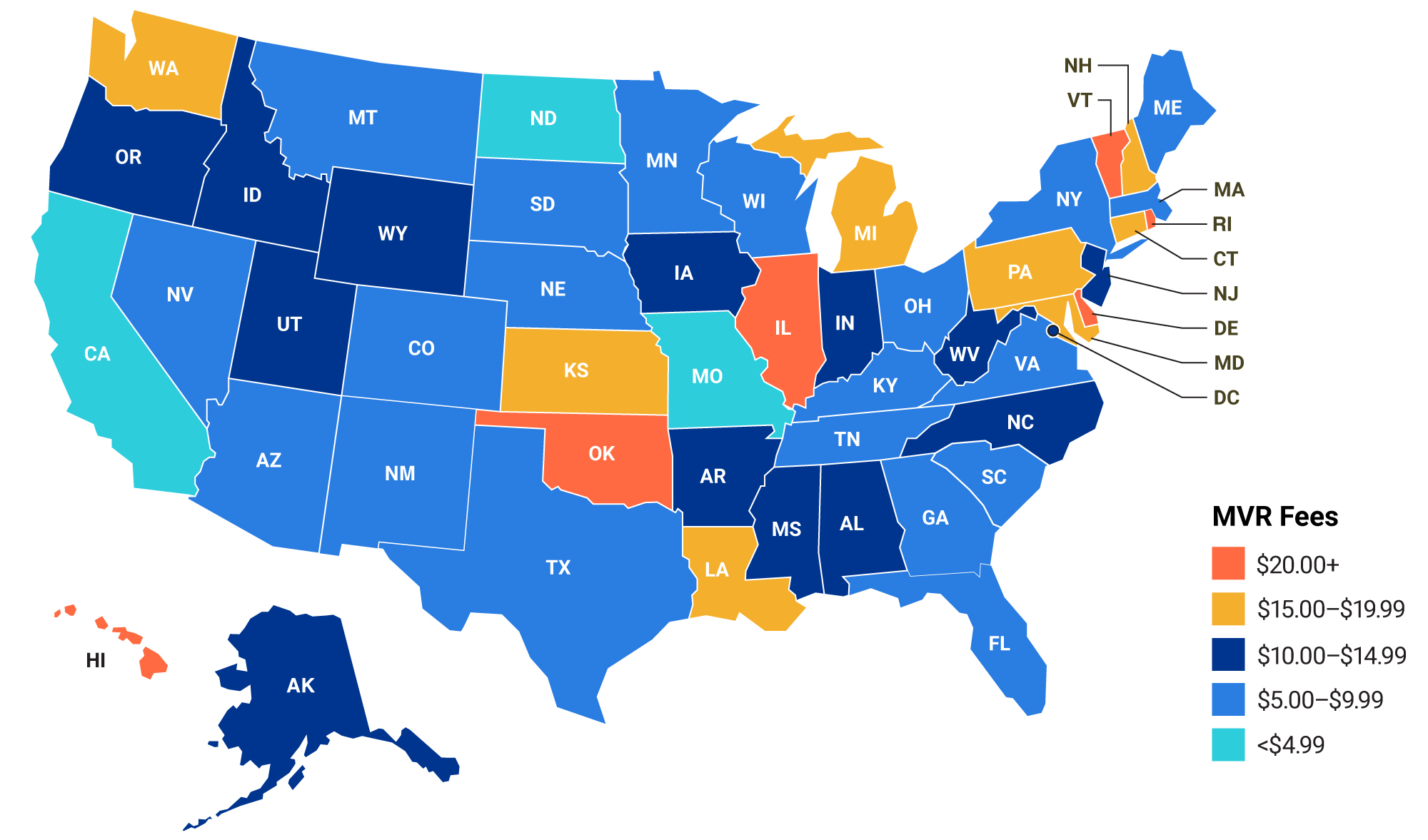

Assessing driving risk is among the costliest aspects of auto insurance underwriting. Even as violations decrease, state motor vehicle report (MVR) fees continue to rise. A new Verisk analysis finds the national average MVR fee has risen to $11.16, an increase of nearly 28% over the past decade.[4]

14 states now charge $15 or more for MVRs[5]

In 2024 alone, MVR fees increase in six states:

- Arkansas, from $11.50 to $12.70

- Colorado, from $2.20 to $6.00

- Maryland, from $12.00 to $15.00

- North Carolina, from $10.75 to $12.75

- Vermont, from $18.00 to $21.00

- Wyoming, from $5.00 to $10.00

The most recent changes bring the number of states that charge $20 or more for MVRs to six, with 14 charging $15 or more.

New advances help confront driving risk—affordably

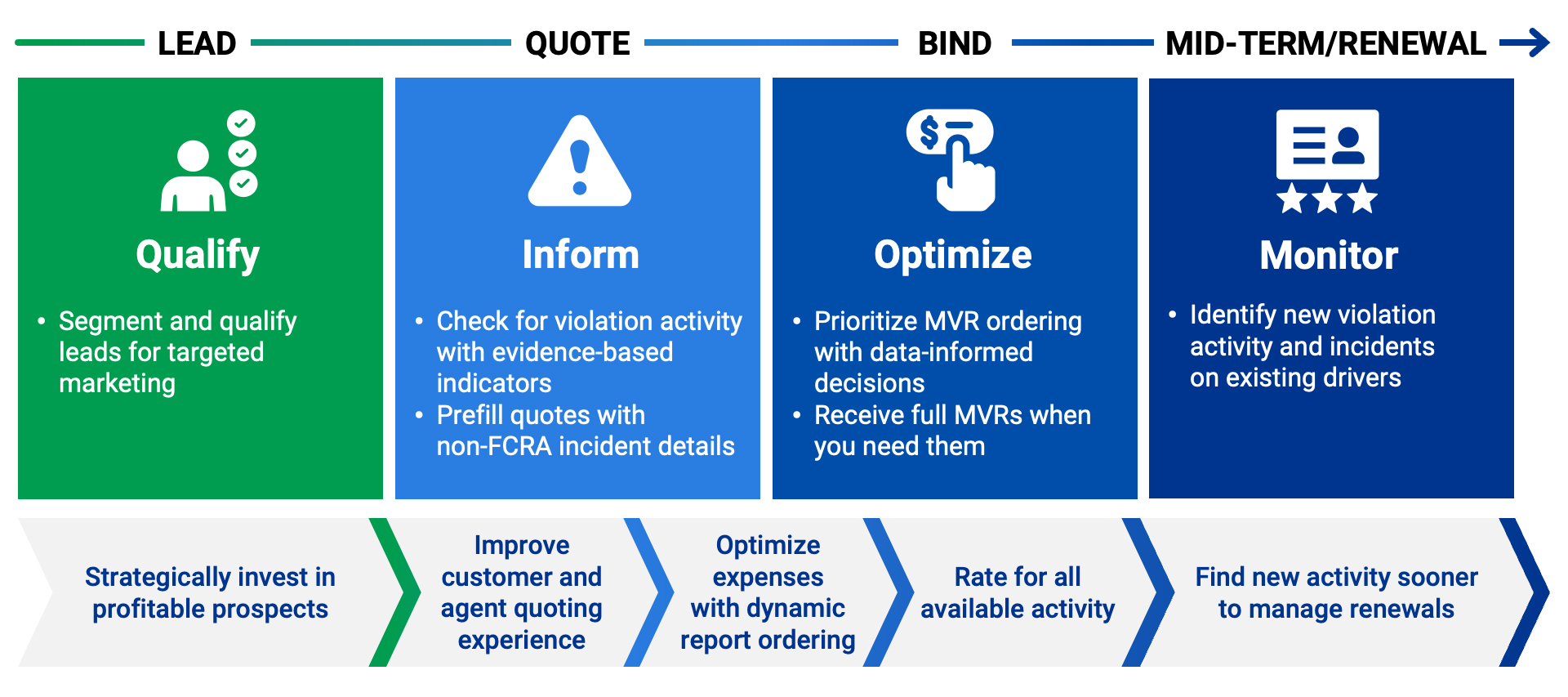

Given the premium leakage, profitability, and safety implications, it’s imperative for auto insurers to track driving risk cost-effectively. Verisk’s Driving History Solutions provide insurers with comprehensive capabilities across the policy life cycle. These tools deliver the most current driving history data on violations and incidents for lead segmentation, initial quoting, mid-term adjustments, and renewals. Cost-saving indicators can support these functions while minimizing unnecessary MVR orders.

Verisk’s Driving History Solutions capabilities across the policy life cycle

The key to MVR expense reduction lies in our unmatched, multisource Public Records IntelligenceTM database with more than 2 billion public records on driver risk, including more than 10,000 connections to traffic courts, more than 300 million crash records, and more than 65 million nontraffic criminal offense records.

Amid ongoing pressure to cut costs, expense optimization continues to be top of mind for many carriers. A suite of tools—providing comprehensive, detailed data with solutions that help maximize information while optimizing cost—improves both accuracy and efficiency.

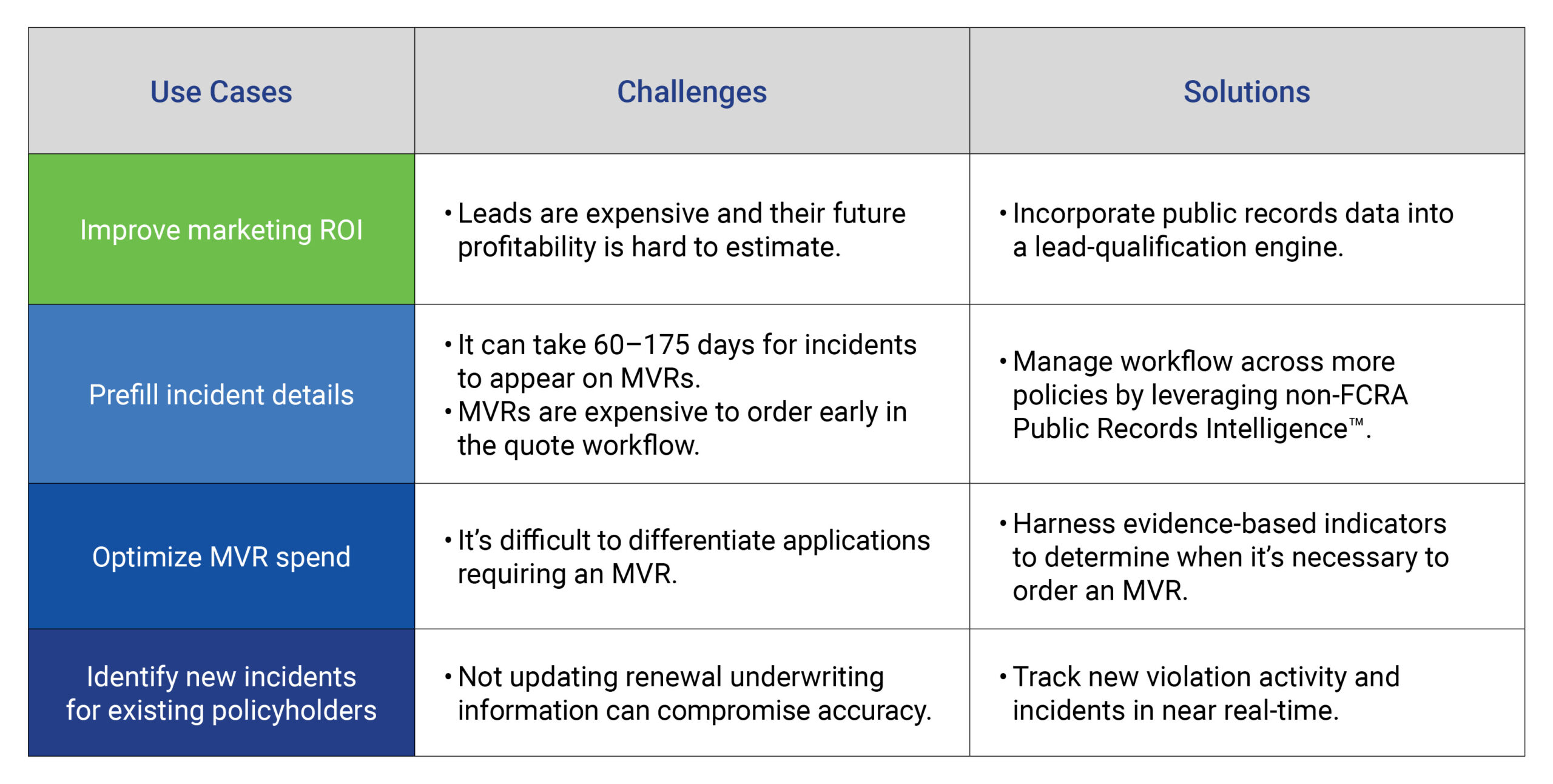

These are examples of information public records can enable insurers to identify:

- Convictions not seen on the MVR

- Violations occurring outside the license state

- New infractions that haven’t yet been placed on the driving record

- Offenses with amended charges

- Details on vehicle crashes

- Nontraffic criminal data, including charges such as financial fraud, offenses related to insurance claims, property damage, and other felony and misdemeanor information

Leveraging court record analytics and data from various public sources, insurers can gain faster risk insights that deliver value across the policy life cycle. These include lead qualification, violation prefill, risk segmentation, optimized MVR ordering, planning future underwriting actions based on incidents not yet adjudicated, and more.

Boost profitability while avoiding premium leakage trade-offs, and save up to 35% with dynamic, integrated solutions that optimize ROI.

Put Verisk to the test. Ask your account executive to schedule a proof-of-concept test of Driving History Solutions.

By Greg Jacobs

Greg Jacobs, director product management, leads product management for Verisk’s auto underwriting solutions. Before joining Verisk, he held several positions in personal and commercial product management with a national carrier. Greg is passionate about developing innovative data and analytics capabilities that help insurers achieve their goals with advanced driving history solutions and valuable use cases for public records intelligence.

Sources:

[1] Updated 2023 estimate based on Coalition Against Insurance Fraud’s The Impact of Insurance Fraud on the U.S. Economy, pages 23-26, applying overall annual premium leakage increase to Verisk’s estimate from The Challenge of Auto Insurance Premium Leakage, 2017.

[2] Early Estimate of Motor Vehicle Traffic Fatalities for the First Half (January-June) of 2024, U.S. Department of Transportation and National Highway Traffic Safety Administration, September 2024; traffic fatalities reached a 20-year high in 2021, and although the rate per 100 million vehicle miles traveled has declined, 2024’s rate remains 9.3% higher than the pre-pandemic 2019 baseline.

[3] Verisk analysis of 157 million court records in AZ, FL, IA, ID, IN, KY, MA, MS, NC, ND, NJ, NM, OK, OR, PA, SD, VA, WA, and WI, 2019-2023, extrapolated to national totals.

[4] Verisk analysis of state motor vehicle report fees as of September 1, 2024.

[5] Ibid.

What Analysts Are Saying About the 2026 P/C Insurance Market

What Analysts Are Saying About the 2026 P/C Insurance Market  Insurance Groundhogs Warming Up to Market Changes

Insurance Groundhogs Warming Up to Market Changes  Modern Underwriting Technology: Decisive Steps to Successful Implementation

Modern Underwriting Technology: Decisive Steps to Successful Implementation  Lessons From 25 Years Leading Accident & Health at Crum & Forster

Lessons From 25 Years Leading Accident & Health at Crum & Forster